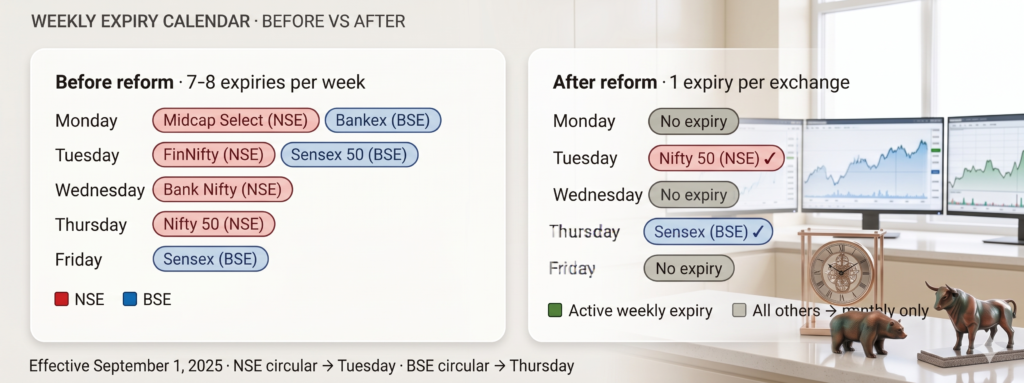

A few years ago, something strange was happening in the Indian stock market. Almost every weekday had an options expiry. Some indices on Monday. Others on Tuesday. Bank Nifty on Wednesday. Nifty on Thursday. Sensex on Friday.

It looked like a busy fish market. Across NSE and BSE, seven or eight different weekly options were expiring every week. For traders, it felt like Diwali for the brokers and a continuous gamble for the small investor.

Then SEBI looked at the damage. And decided the party had to end.

The number that shocked everyone

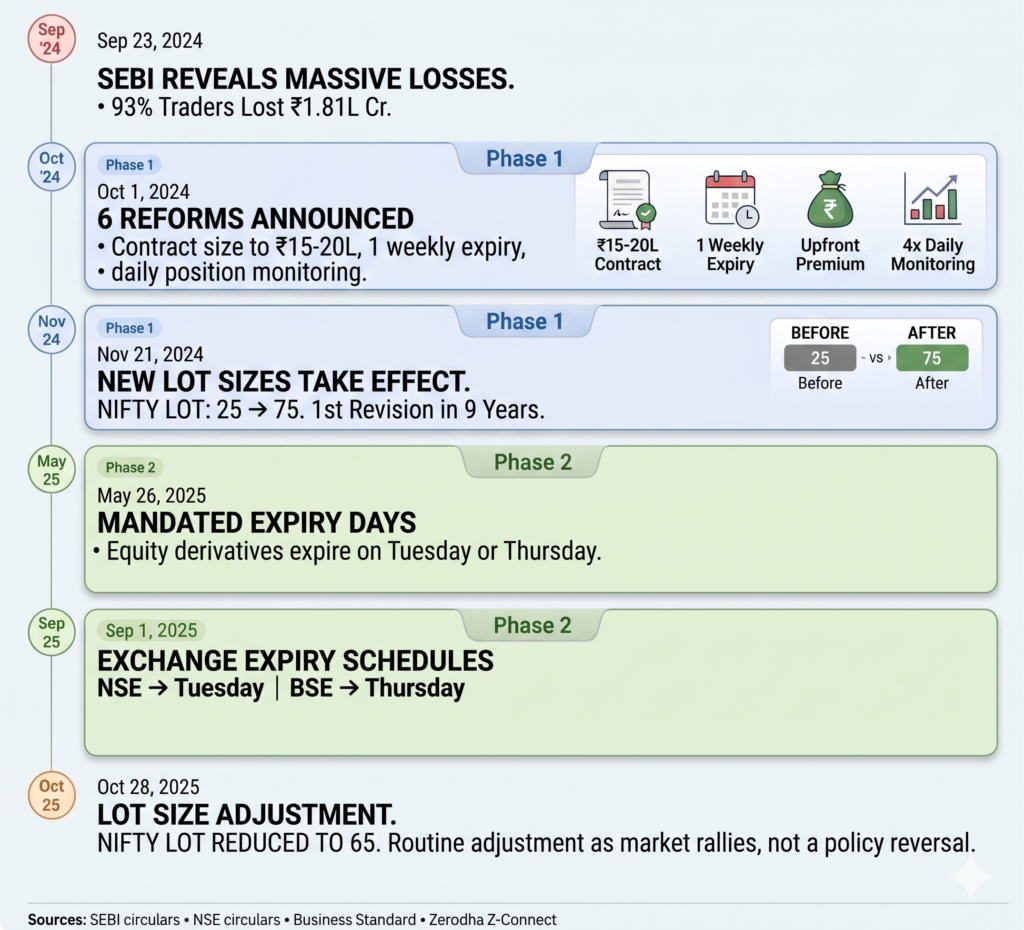

In September 2024, SEBI dropped a study that made the whole industry go silent. Between FY22 and FY24, 93 percent of individual traders in India’s F&O market had lost money. Total losses crossed ₹1.81 lakh crore. That is more than the entire annual budget of many Indian states.

Only about 7 out of every 100 traders made any profit. And most of the money that small traders lost went to one place. Big institutional players. Foreign funds. Algorithmic traders. Computers that ran thousands of trades per second.

This was not normal market risk. It looked more like a quiet, steady transfer of wealth from kitchens and middle class savings into the pockets of machines. Every week. On multiple expiry days.

SEBI could not look away anymore.

What SEBI actually did

SEBI’s response came in two big steps.

Phase one came in October 2024. Through its circular dated October 1, 2024, the regulator pushed up the minimum size of an index F&O contract from ₹5 to ₹10 lakh to a new range of ₹15 to ₹20 lakh. This was the first such change in nine years.

That meant lot sizes had to be increased. Nifty, which used to trade in lots of 25, jumped to a lot size of 75 from late December 2024. Each trade now needed much more capital. The casual small trader could no longer enter F&O with pocket change.

In the same phase, SEBI also cut down the number of weekly expiries. Each exchange could now offer only one weekly expiry, and only on its main index. NSE kept Nifty 50. BSE kept Sensex. Bank Nifty, FINNIFTY, Midcap Select, Bankex and others were moved to monthly expiry only. The daily expiry chaos slowly began to settle.

From February 2025, SEBI also forced option buyers to pay the full premium upfront. Position limits were checked four times a day instead of once. The free-for-all was being cleaned up.

Phase two came in May 2025. Through circular SEBI/HO/MRD/TPD-1/P/CIR/2025/76 dated May 26, 2025, SEBI did something even more historic. It said every exchange must choose just one fixed day for weekly expiry. The only options were Tuesday or Thursday.

NSE picked Tuesday. BSE picked Thursday. From September 1, 2025, this came into force. With that, NSE quietly ended its 25-year-old tradition of Thursday expiry. Old habits had to die.

There was one more small but interesting twist. As Nifty kept rising through 2025, the contract value at the lot size of 75 crossed the ₹20 lakh ceiling. So NSE reduced Nifty’s lot size to 65 through a circular dated October 3, 2025, taking effect with the January 2026 expiries. This was not a softening of the rules. It was the system simply adjusting because the market had moved up.

Is it actually working?

This is where the honest answer gets a bit tricky.

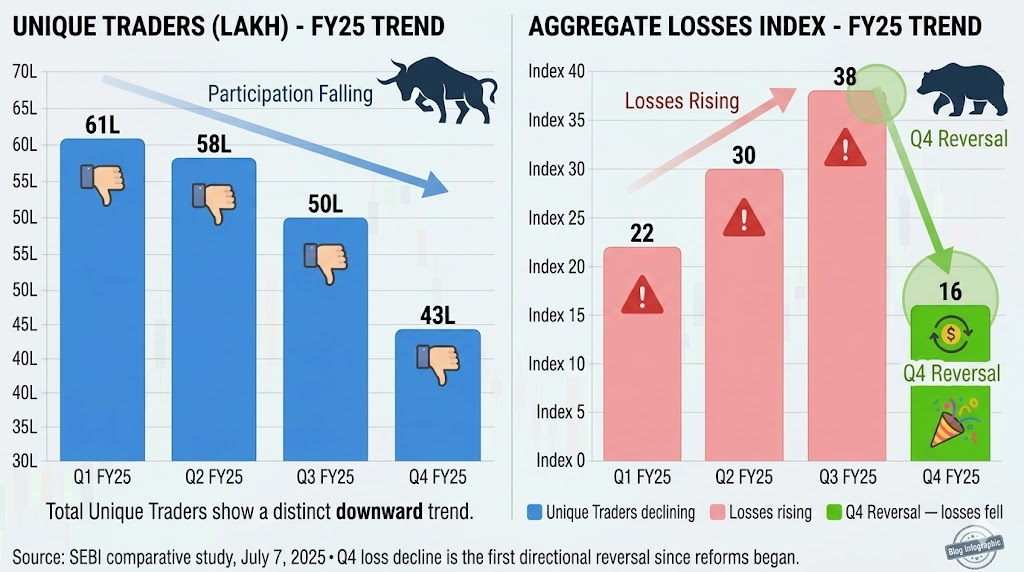

The FY25 numbers, released by SEBI in July 2025, looked grim at first glance. Net losses of individual F&O traders jumped 41 percent year on year, from ₹74,812 crore in FY24 to a painful ₹1,05,603 crore in FY25. The average loss per trader rose from ₹86,728 to about ₹1.1 lakh. About 91 percent of traders still ended the year in the red.

A casual reader would say SEBI’s reforms have failed. But the full-year number hides the real story.

Look more closely. The number of unique individual traders fell sharply within FY25 itself. From 61.4 lakh in the first quarter to 42.7 lakh in the fourth quarter. That is a 30 percent drop in just one year.

In the six months from December 2024 to May 2025, the period right after SEBI’s reforms kicked in, individual traders’ turnover in equity derivatives dropped 11 percent. Index options notional volume fell 29 percent. Premium turnover fell 9 percent.

And here is the most important line in SEBI’s own July 2025 study. For the first three quarters of FY25, losses kept climbing. But in the fourth quarter, losses actually came down. That was the first quarterly reversal since the reform began.

In simple words, FY25 looked bad on paper because the damage was already done in the first half. By the time SEBI’s full reform stack was in place, the bleeding had started to slow.

The honest counter view

There is one fair point that critics raise. Even though the number of traders fell, the average loss per remaining trader actually went up. Fewer people in the game, but each one losing more.

That is not a small thing. It tells us the casual punters left the table, but the more aggressive ones doubled down. SEBI will need full FY26 data to truly prove that per-trader losses are also falling. Until then, the reform is a work in progress.

This is also where many retail participants begin searching for a reliable short term stock advisor India instead of blindly entering leveraged weekly options trades. The shift from speculative gambling toward disciplined trading and risk management may ultimately be one of the unintended benefits of SEBI’s crackdown.

What this means for you

If you are an investor or trader, these changes matter in a very practical way.

The market is now structurally calmer around expiry. With most indices on monthly contracts and only Nifty and Sensex on weekly expiry, sharp price swings on random weekdays have reduced. Underlying stocks can trend more freely without daily options pressure pulling them around.

For those who follow Swing stock trading advice in India, the new fixed Tuesday and Thursday expiry calendar gives a clean rhythm. You know exactly when options activity will peak. You can plan entries and exits around it. That predictability is a quiet gift.

For long term investors, the bigger benefit is even simpler. Less noise. Less manipulation around expiry day. A market that is slowly being shifted from a daily casino back to a place where capital can actually form.

The bigger picture

Stepping back, what SEBI has done is more than a rule change. It is one of the most decisive retail protection moves any Indian regulator has made in decades.

The regulator did not act because the market was too speculative. Speculation is part of any market. SEBI acted because the speculation was structurally tilted against the small Indian saver. Tilted by design. Tilted by daily expiries, tiny lot sizes, and rules built for institutional players.

The Q4 FY25 reversal is the first proof that the tilt has begun to correct. FY26 will tell us whether the correction holds.

For now, the simplest way to read this story is this. SEBI looked at lakhs of Indians quietly losing their savings every Thursday. And said, no more.

That alone makes this one of the most important reforms of this decade.