Margin of safety is the simple but powerful idea of buying stocks for much less than what they are really worth, so that even if you are wrong, your downside is limited—and if you are right, your upside can be meaningful. At its core, it is your personal safety net against mistakes, volatility, and bad luck in the stock market.

What is margin of safety?

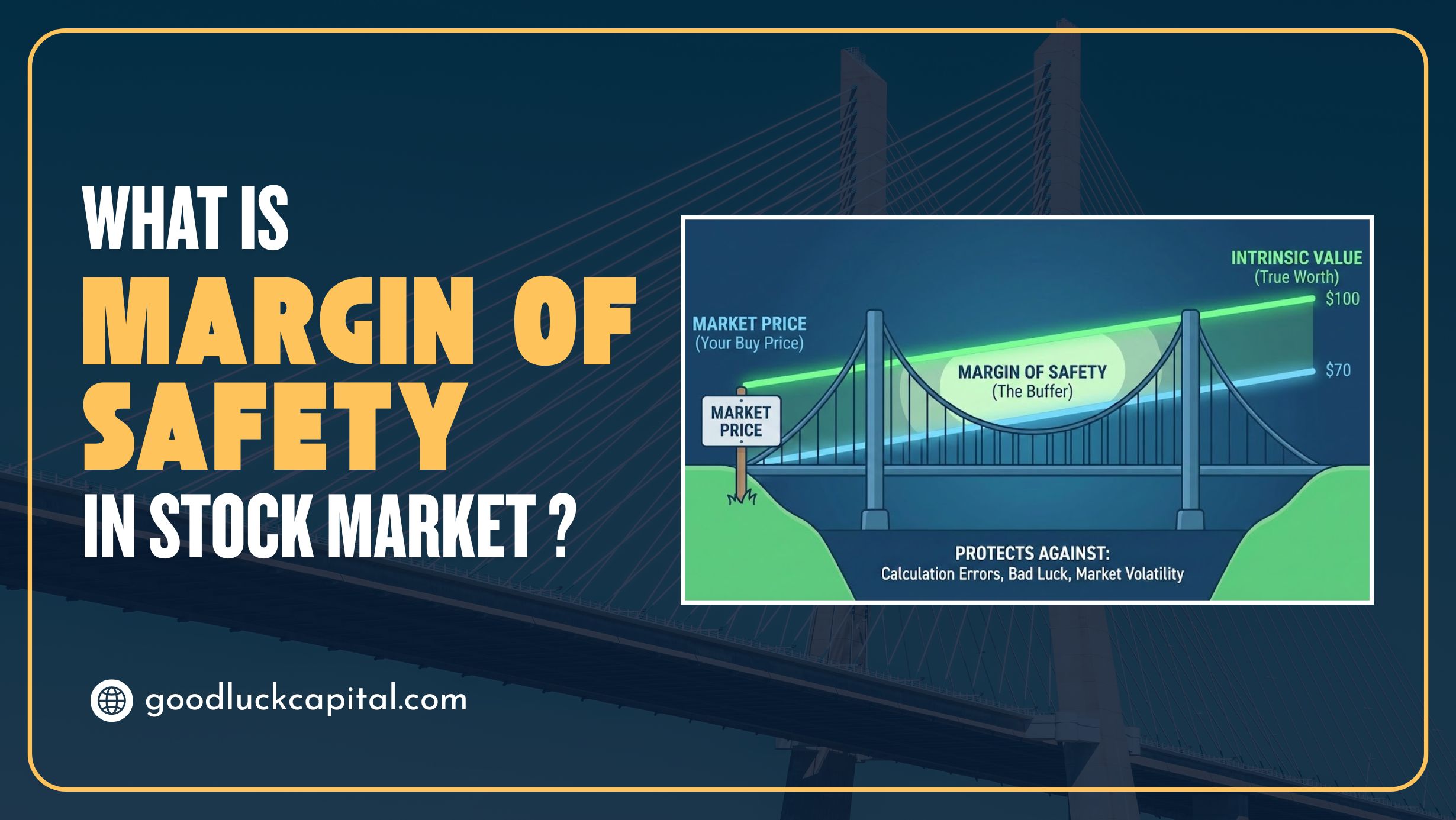

In investing, margin of safety is the gap between a stock’s intrinsic value (what the business is really worth) and its current market price. If you believe a company is worth 100 per share and you can buy it at 70, your margin of safety is 30%.

Benjamin Graham and David Dodd introduced this concept in their classic book “Security Analysis” and later in “The Intelligent Investor,” calling it the central principle of sound investing. Their insight was straightforward: because intrinsic value is always an estimate and the future is uncertain, you should never buy a business at its full estimated value—always demand a discount.

Margin of safety vs accounting usage

You may also see “margin of safety” used in management accounting, where it means how far sales can fall before a business hits break-even. That is useful for managers, but it is different from what equity investors mean.

In the stock market, margin of safety strictly refers to buying when market price is well below intrinsic value, creating a buffer against valuation errors and market shocks. Think of it as buying a strong company at a bargain price, so that you have room for bad news, slow growth, or just plain forecasting mistakes.

Why it matters for everyday investors

Markets are influenced by interest rates, macro headlines, sector cycles, liquidity flows, and crowd psychology—all of which can cause sharp swings in prices even for fundamentally sound companies.

No investor—whether retail participants, institutions, or even a SEBI registered stock trading advisor—can predict market movements with perfect accuracy. Because forecasting is inherently uncertain, margin of safety becomes a practical risk-management tool.

Interestingly, the principle also applies beyond long-term value investing. Even in swing trading advice, disciplined traders look for setups where potential downside is limited compared to potential upside. While swing trading focuses more on technical structures, the underlying philosophy—protect capital first—remains the same.

How to think about intrinsic value

Intrinsic value is an estimate of what a business is really worth based on its cash flows, earnings power, and assets—not today’s share price. Common ways to estimate it include:

- Discounted cash flow (DCF) models

- Earnings-based valuation (normalized earnings times a reasonable multiple)

- Conservative asset-based or liquidation value for asset-heavy or cyclical businesses

Professional guides emphasize that intrinsic value is a range, not a precise number, because future cash flows and discount rates are uncertain. That uncertainty is exactly why Graham, Buffett and others insist on a margin of safety instead of paying “fair value.”

The basic margin of safety formula

A simple way to express margin of safety in stocks is:

Margin of Safety = (Intrinsic Value − Market Price)/ Intrinsic Value

If you think a stock is worth 200 and it trades at 120, the margin of safety is (200 – 120)/200 = 40%. Many value-investing resources suggest working with discounts in roughly the 20–50% range—larger when uncertainty is high, smaller when the business is extremely stable and predictable.

How much margin of safety is enough?

The “right” margin of safety depends on business quality, earnings stability, balance sheet strength, and your own risk tolerance. Global guides generally agree that higher uncertainty (turnarounds, small caps, cyclicals) demands a higher margin of safety than steady, dominant franchises.

For very stable, cash-generating businesses with durable competitive advantages, investors may accept a lower margin of safety because earnings and cash flows are easier to forecast. For more volatile or complex companies, many practitioners look for 40–50% or greater discounts to intrinsic value to compensate for forecasting risk.

A practical step-by-step framework

Here is a simple way a long-term investor can apply margin of safety in everyday stock selection:

1. Start with business quality

Focus on understandable businesses with clean accounts, reasonable leverage, and a track record of profits and cash flows. Margin of safety works best when the underlying business is at least decent; it cannot save you from outright fraud or a terminally dying industry.

2. Estimate conservative intrinsic value

- Use normalized earnings and a reasonable P/E multiple based on sector history, or

- Do a simple DCF with modest growth and conservative margins, or

- Use a conservative asset-based value for cyclical or asset-heavy names.

Guides consistently stress using conservative inputs rather than heroic growth assumptions.

3. Decide your required margin of safety

- Stable, predictable compounders with strong balance sheets: lower MOS (say around 20–30%).

- Mid/small caps, cyclicals, turnarounds: higher margin of safety (often 40–50% or more) to compensate for greater uncertainty.

4. Check the current market price

Buy only if the current price is meaningfully below your intrinsic value estimate by at least your chosen margin of safety. If the price is too close, be patient—many investor-education sources highlight waiting, not forcing trades at insufficient discounts, as a core discipline.

5. Revisit your thesis periodically

As new results, regulations, or sector changes emerge, update your intrinsic value and see if your margin of safety still exists. If the price has moved up and margin of safety has disappeared, consider whether the stock has simply reached fair value.

A quick numerical example

Suppose you analyse a mid-cap company and estimate its intrinsic value at 500 per share using conservative earnings and a sector-appropriate multiple. Because it has some earnings volatility, you decide you want at least a 40% margin of safety.

A 40% margin of safety means you would be comfortable buying only if:

Buy Price ≤ Intrinsic Value × (1 − 0.40) = 500 × 0.60 = 300

If the stock trades at 420, you simply pass or wait; if it corrects to around 300 while fundamentals remain intact, it enters your buy zone. This discipline helps you avoid overpaying during bull-market euphoria, which many educational articles warn against.

Common mistakes investors make

A frequent mistake is treating any low P/E or “cheap-looking” stock as having a margin of safety, without carefully estimating intrinsic value or understanding business quality. Low valuations can reflect genuine problems—poor governance, declining industry, or unsustainable earnings—turning apparent bargains into value traps.

Another common error is using over-optimistic assumptions for growth and margins, which inflates intrinsic value and gives a false sense of safety. Guides stress using conservative, reality-checked inputs precisely because the future is hard to forecast.

Finally, many investors rely completely on pre-built calculators or broker reports without doing their own thinking on management quality, balance sheet strength, and industry dynamics. Tools and ready-made intrinsic values are useful starting points, but your true margin of safety exists only if you understand and trust the assumptions behind those numbers.

Final Thoughts

Margin of safety is not a shortcut to quick profits. It is a mindset of discipline, patience, and respect for uncertainty.

The principle introduced by Benjamin Graham remains timeless: never pay full price when your valuation is only an estimate.

Whether you are a long-term value investor building wealth steadily, someone learning structured research methods, or even a trader applying disciplined swing trading advice, the core principle remains unchanged:

Protect capital first. Demand favorable risk–reward. Let upside follow naturally.

In uncertain markets, margin of safety is not optional—it is essential.