You sold a stock. You made a profit.

Before you celebrate, one question matters.

How much of that profit actually belongs to you?

Let’s find out. No complicated terms. No confusing numbers. Just the plain truth.

Think of it like this

The government looks at two things when you sell a stock.

One. How long did you hold it?

Two. How did you trade it?

Based on those two answers, your tax is decided. That’s the whole framework. Everything else is just details.

This is something every investor, especially those looking for short term stock trading advice in India, should understand before focusing only on profits.

You held the stock for more than a year

Good news.

You pay a lower tax. Just 12.5% on your profit.

Even better news.

The first ₹1.25 lakh of that profit is completely free. No tax at all.

So if you made ₹80,000 in profit after holding a stock for over a year?

You pay nothing.

If you made ₹2,00,000?

You only pay tax on ₹75,000. That is the amount left after subtracting ₹1.25 lakh.

Tax = ₹75,000 multiplied by 12.5% = ₹9,375.

That’s it. Not more.

You held the stock for less than a year

The tax is higher here. 20% on your profit.

No free limit this time.

So if you made ₹50,000 and held the stock for 8 months, you pay 20% on the full amount.

A smart thing to do every March

Imagine you have built up ₹1 lakh in long-term profit across some stocks.

Before March 31, you can sell those stocks and pay zero tax on the profit. Because it is under ₹1.25 lakh.

Then you buy the same stocks again the next day.

Fresh start. New price. New year. New free limit.

This is completely legal. Many smart investors do it every year.

Many experienced investors and even a SEBI registered stock trading advisor suggest this as a simple tax saving strategy.

You traded the same stock within one day

This is called intraday trading.

And here, the rules change completely.

The government does not treat this as investing. They treat it as running a small business.

So your profit is added to your total income for the year. And taxed like your salary.

If you earn enough to be in the 30% tax bracket, your intraday profits are taxed at 30%.

Also, you must file a different tax form called ITR-3.

You trade futures and options

This is also treated like a business, similar to intraday.

Your profits are added to your income and taxed at your slab rate.

You also need to file ITR-3.

The one advantage here is that if you made a loss in F&O, you can use that loss to reduce tax on other income in future years. For up to 8 years.

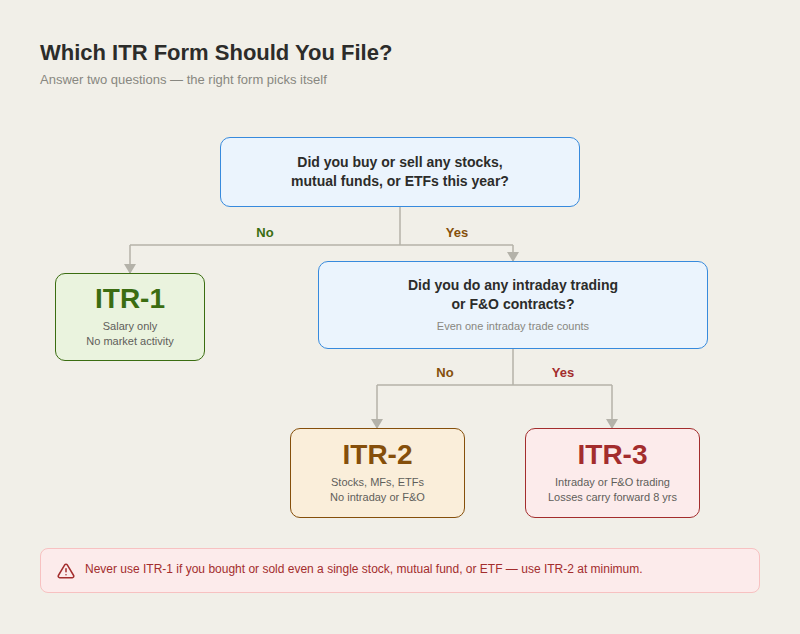

Which form do you file?

Think of it this way.

You only invest in stocks and hold them. Use ITR-2.

You also do intraday trading or F&O. Use ITR-3.

You have no stocks at all. Use ITR-1.

Never use ITR-1 if you have bought or sold even one stock in the year.

Three things that get people into trouble

One. Not checking your AIS.

AIS is a document on the Income Tax website. It shows every stock transaction you made that year. The government already has this data from your broker.

If what you file doesn’t match this, you get a notice.

Check it before you file. Every year.

Two. Not filing when you made a loss.

Even a bad year needs a return filed.

If you don’t file, you lose the ability to use that loss to reduce tax in future years.

File anyway. It protects you later.

Three. Forgetting dividend income.

Dividends are taxable now. They get added to your income and taxed at your slab rate.

If you received dividends and didn’t mention them, the tax department already knows. It’s in your AIS.

The whole thing in one simple table

| What you did | Tax you pay | Form to file |

|---|---|---|

| Held stock for over 1 year | 12.5% on profit above ₹1.25 lakh | ITR-2 |

| Held stock for under 1 year | 20% on full profit | ITR-2 |

| Intraday trading | As per your income slab | ITR-3 |

| F&O trading | As per your income slab | ITR-3 |

The one habit that saves you money every year

Before March 31, check your long-term profits.

If they are close to ₹1.25 lakh, sell and buy back.

Pay zero tax. Reset the clock.

Do it every year.

Over 10 years, this small habit can save you more money than you expect.