On April 26, 2026, Sun Pharma announced it will acquire a company called Organon for $11.75 billion.

All cash.

This is the largest overseas acquisition ever made by an Indian pharmaceutical company. Not just pharma. Any Indian company. Ever.

If you follow Indian markets, you need to understand what happened, why it happened, and where the risk is.

What actually happened

Organon is a US-based company spun off from the pharmaceutical giant Merck in 2021. It focuses on three things: women’s health medicines, biosimilars, and established branded drugs.

For the year ending December 2025, Organon earned revenue of $6.2 billion and generated over $1 billion in free cash flow.

Here is the part that stops you in your tracks.

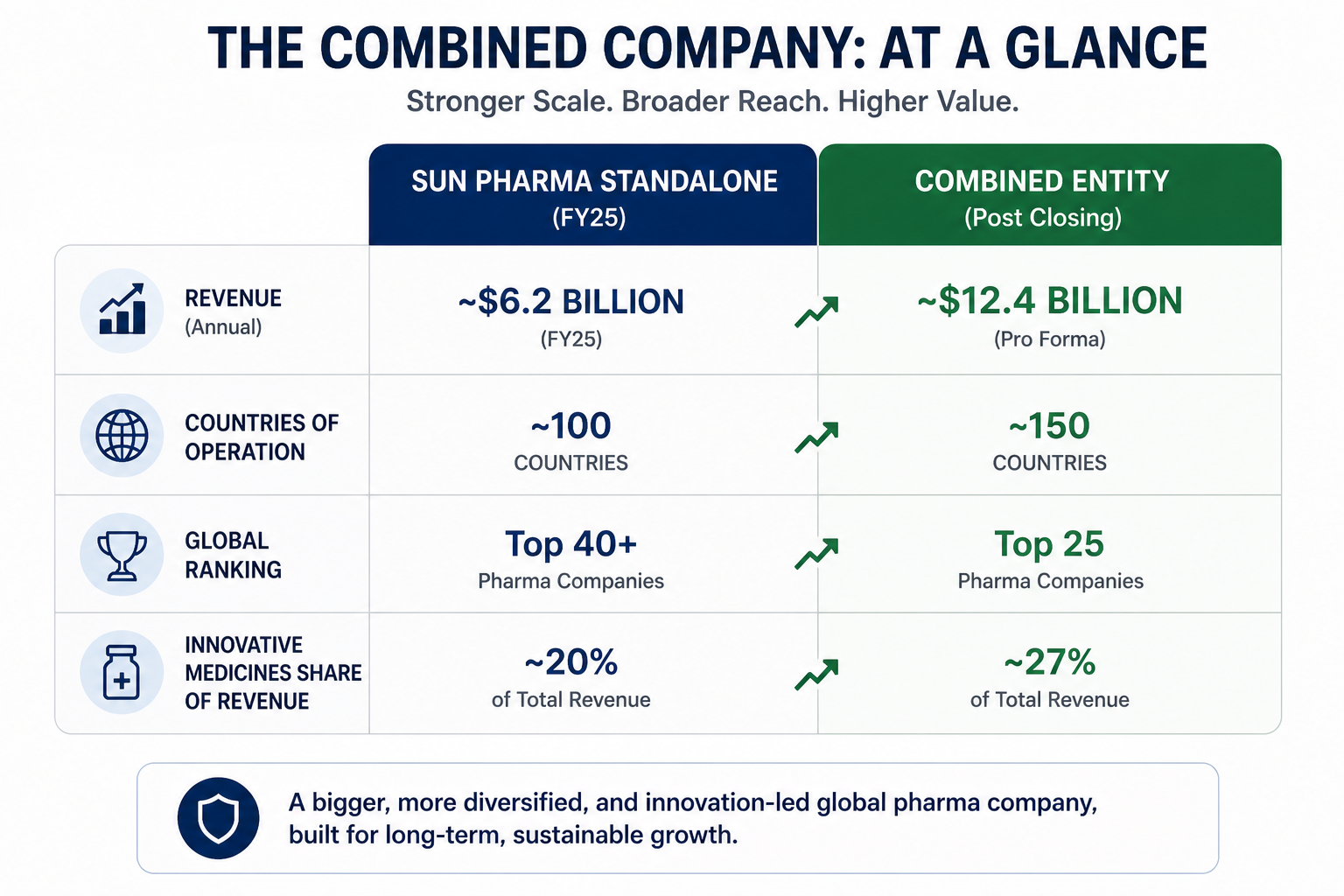

Sun Pharma’s own revenue in FY25 was also around $6.2 billion.

They just bought a company their own size.

Why Sun Pharma did this

Sun Pharma is India’s largest pharma company.

But there was a quiet problem building for years.

Their main business is generic medicines. Generics are a commodity. Paracetamol is paracetamol. Any manufacturer can make it. The only competition is price.

In the US, that price competition had become brutal. Buyers switch suppliers the moment someone offers a cheaper quote. Margins shrink. Growth slows.

Sun Pharma needed to move into higher-value medicines. Products where brand, patents, and innovation matter more than just price.

Building that from scratch takes 10 to 15 years.

So they took a shortcut. They bought Organon.

For long-term investors and anyone searching for the best stock advisor in India, this acquisition marks a strategic shift from low-margin generics toward premium global healthcare businesses.

Three things they actually got

Women’s health leadership.

Organon is the second largest company in the world for contraceptive medicines and third largest in fertility medicines.

Sun Pharma became a top-3 global player in women’s health overnight.

This market is very different from generics. People stick to what works. Doctors recommend trusted brands. Pricing power is real.

Biosimilars at scale.

Biosimilars are complex medicines produced after a patent expires on a biological drug. They are the next big wave in pharma.

After this acquisition, Sun Pharma becomes the 7th largest biosimilar company in the world.

Global reach.

Before this deal, Sun Pharma operated in around 100 countries. After Organon, that grows to approximately 150 countries. With 18 individual markets each generating over $100 million in annual revenue.

Building that kind of global network from scratch would have taken many years.

What the combined company looks like

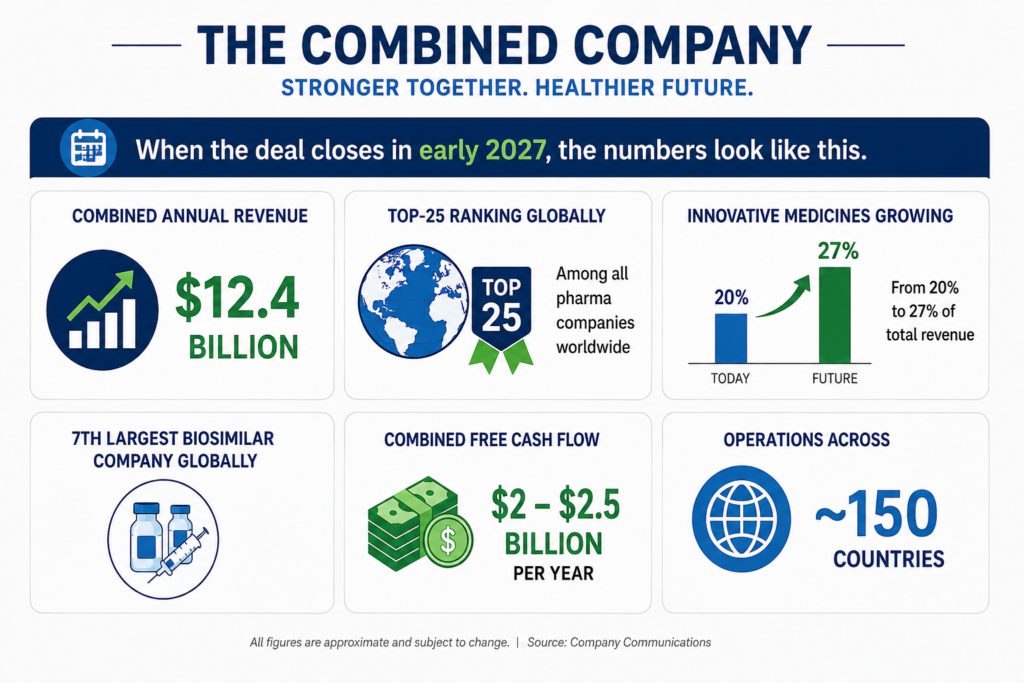

When the deal closes in early 2027, the numbers look like this.

Combined annual revenue of $12.4 billion. A top-25 ranking among all pharma companies worldwide. Innovative medicines growing from 20% to 27% of total revenue. The 7th largest biosimilar company globally. Combined free cash flow of $2 to $2.5 billion per year. Operations across roughly 150 countries.

Sun Pharma shares jumped 7% on the day of the announcement. Organon shares jumped 17%.

Markets liked it.

The risk, and it is a real one

Nothing this big comes without a cost.

Before this deal, Sun Pharma had more cash than debt. That is a rare and comfortable position for any large company.

After closing, that changes completely.

The combined company will carry a net debt to EBITDA ratio of 2.3 times.

That is not a crisis. But it is a major shift. And it means one thing clearly.

Execution cannot fail.

Organon itself had $8.6 billion in existing debt at the end of 2025. That comes along with the acquisition.

The second risk is integration.

Two large companies. Two different cultures. One based in India and one in New Jersey. Different systems, different ways of working, different people.

History shows that two out of every three acquisitions fail to deliver the benefits promised at the time of announcement.

That does not mean this deal will fail. Sun Pharma has a track record of successfully absorbing acquisitions over the years. But investors should watch integration progress closely after 2027.

What this means for Indian pharma overall

This deal sends a clear signal to the world.

Indian pharma is not just a cheap generic medicine supplier anymore.

It can now acquire global companies, enter premium markets, and compete at the highest levels of world pharma.

It also tells you something important about where the industry is headed.

The plain generic business has limited room to grow. US price pressure, global competition, and commoditisation are real and ongoing.

The companies that succeed in the next decade will be the ones that move into specialty medicines, biosimilars, and innovation.

Sun Pharma just made that move in a single transaction.

Conclusion

The problem was clear. Sun Pharma’s US generic business was under price pressure with no quick fix in sight.

The solution was bold. Buy Organon and gain scale, global reach, and premium market exposure all at once.

The outcome on paper is impressive. A $12.4 billion revenue company, ranked top 25 in the world, top 3 in women’s health, and top 7 in biosimilars.

The risk is equally real. Over $9 billion in new debt and the complexity of merging two large companies across 150 countries.

The verdict is this. Strategically it makes sense. Financially it is heavy. And execution is everything.

For investors looking for deeper market insights, sector analysis, and long-term opportunities, following a reliable SEBI registered stock advisory can help separate temporary market excitement from real long-term value creation.

When the deal closes in early 2027, that is when the real story begins.

Watch closely.