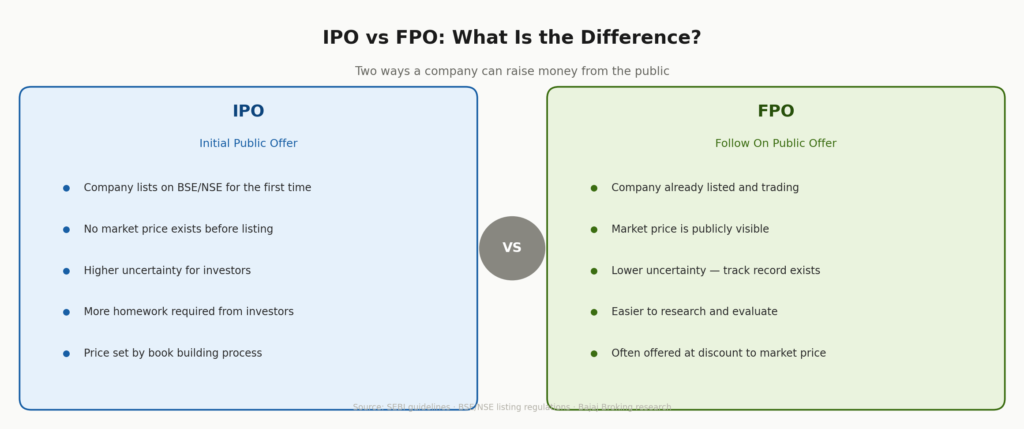

Most Indian investors know what an IPO is. A company comes to the stock market for the first time, offers its shares to the public, raises money, and gets listed. There is buzz, subscription data, grey market premiums, and excitement all around.

But what happens when that same company, already listed and trading every day, decides it needs more money from the public again?

That is where the FPO comes in.

So what exactly is an FPO?

FPO stands for Follow On Public Offer. In the simplest possible words, it is when a company that is already listed on BSE or NSE decides to sell more shares to the public.

Think of it this way. A company held its IPO, raised funds, got listed, and has been running for a few years. Now it wants to expand into a new business. Or pay down a large loan. Or the government wants to reduce its stake in a public sector company. Whatever the reason, the company needs more capital. And one of the ways it can raise that capital is by going back to the public and offering more shares.

That process is the FPO. It is essentially a second round of public fundraising. The company is already known. Its financials are public. Its track record is visible. Investors do not have to guess about the business the way they do with an IPO.

For investors who actively follow stock recommendations for short term, an FPO can also become an important event to watch, especially when a fundamentally strong company raises capital to support its next phase of growth.

The two types of FPO every investor must know

Not all FPOs work the same way. There are two completely different types and understanding the difference matters a lot before you decide to invest.

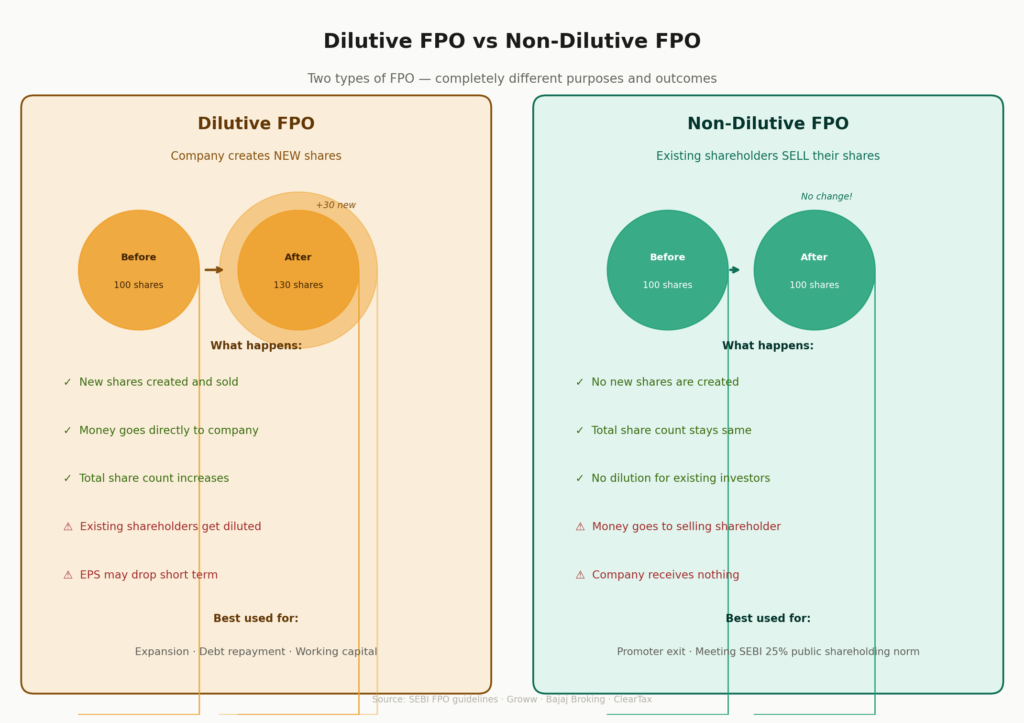

The first type is called a dilutive FPO. Here the company creates brand new shares and offers them to the public. More shares means more money coming into the company. But it also means the total number of shares in the market increases. When the total shares go up but the company’s profit stays the same for now, each share represents a slightly smaller piece of the pie. This is called dilution. Existing shareholders find their ownership percentage slightly reduced.

A dilutive FPO makes sense when the company genuinely needs fresh capital for growth, debt repayment, or expansion. The money raised goes directly into the company.

The second type is called a non-dilutive FPO. Here, no new shares are created at all. Instead, an existing large shareholder, usually a promoter or the government in case of public sector companies, sells some of their own shares to the public. The company itself does not receive any of this money. The selling shareholder does. The total number of shares in the market stays exactly the same.

A non-dilutive FPO is typically used when a promoter wants to reduce their stake, or when a listed company needs to comply with SEBI’s minimum public shareholding requirement of 25 percent.

Real Indian examples that make this clear

India has seen several significant FPOs over the years. Each one had a different story behind it.

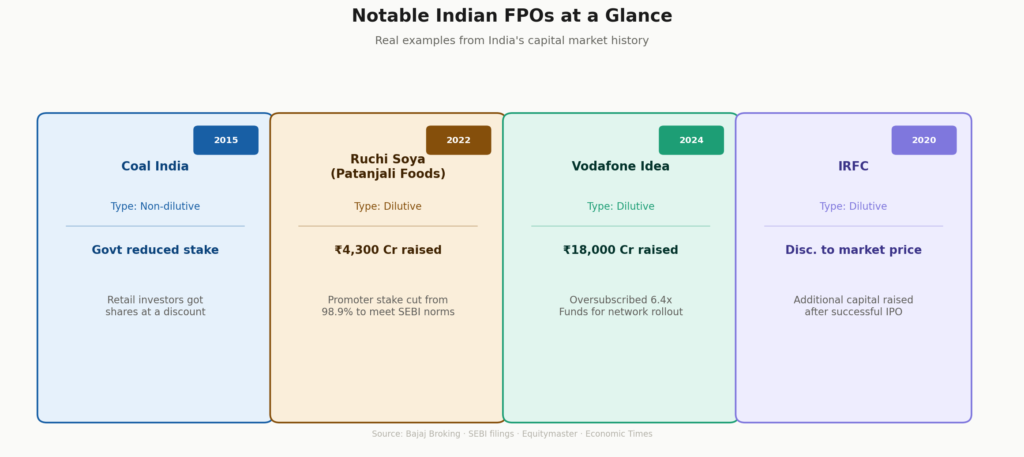

Coal India is one of the most cited examples of a government-led FPO. After listing through an IPO, the government sold additional shares to the public to reduce its own stake and meet regulatory norms. Retail investors were offered shares at a discount. It became one of the most subscribed FPOs in Indian history.

Ruchi Soya Industries, which was later rebranded as Patanjali Foods, ran a notable FPO in 2022. The promoter’s stake was an extremely high 98.9 percent, far above what SEBI permits. The company launched a Rs 4,300 crore FPO specifically to reduce that stake and bring public shareholding up to the required level. The FPO was fully subscribed and shares listed roughly 36 percent above the issue price.

The Vodafone Idea FPO of 2024 was one of the largest ever in India. The company raised Rs 18,000 crore through a dilutive FPO to fund its network expansion and reduce its enormous debt burden. Despite its financial struggles being well known, the FPO was oversubscribed approximately 6.4 times, showing that investors were betting on a turnaround.

IRFC, the Indian Railway Finance Corporation, also ran an FPO after its IPO to raise additional capital, offering shares at a discount to the prevailing market price.

How does the FPO process actually work?

The process follows steps similar to an IPO, but slightly simpler because the company is already listed and its information is already publicly available.

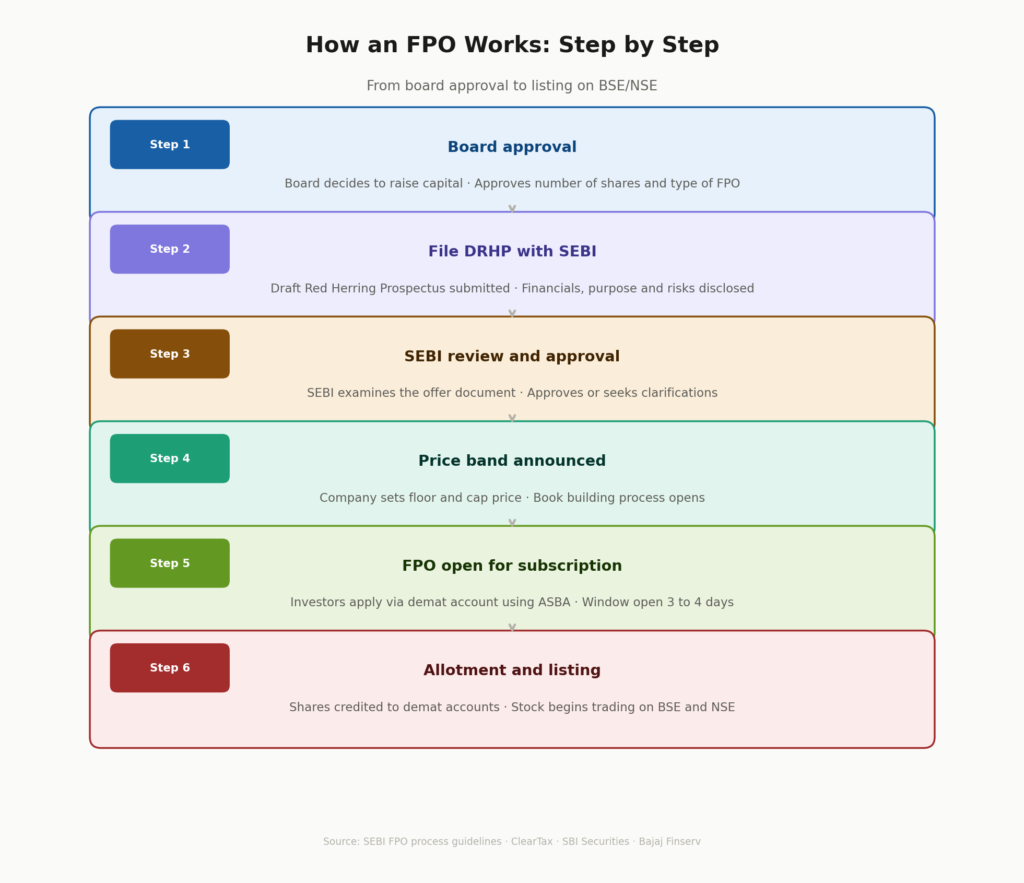

First, the company’s board approves the decision and decides how many shares to offer and why. Then the company files a Draft Red Herring Prospectus, or DRHP, with SEBI. This document contains all the key details including financial history, purpose of the fundraise, number of shares, and price band.

Once SEBI approves, a final Red Herring Prospectus is published. The FPO opens for public subscription, typically for three to four days. Investors apply through their demat accounts using the ASBA process, exactly as they would for an IPO. After the offer closes, shares are allotted and credited to investors’ accounts. Trading begins shortly after.

Should you invest in an FPO?

Like any investment, the answer depends on the company and the purpose behind the FPO.

A dilutive FPO where the money is being used to fund genuine expansion or reduce debt in a fundamentally strong company can be a good opportunity. The investor is essentially buying into the company’s next growth phase.

A non-dilutive FPO where an existing shareholder is simply selling out tells you nothing new about the company’s growth plans. The company itself receives nothing. Evaluate it purely on whether the price makes sense for the business.

Always read the RHP before applying. The document clearly states what the money will be used for. While many investors also look for expert share market tips before participating in an FPO, understanding the company’s use of funds should always be the starting point. A company raising capital to expand capacity is very different from one raising funds simply to cover operating losses.

Check the company’s existing debt levels, profit consistency, and how realistic the stated use of funds actually is. FPOs are generally less risky than IPOs because years of financial data are publicly available. But less risky does not mean risk-free.

A simple closing thought

The FPO is one of the most practical tools in the Indian capital market. For companies, it is a way to raise fresh capital without the full complexity of a new listing. For investors, it is a chance to buy into a known company at a defined price with much more information available than any IPO ever provides.

Understanding the difference between dilutive and non-dilutive, reading why the company is raising money, and comparing the FPO price with the current market price are the three simple checks that separate a smart FPO decision from a careless one.

The name sounds complicated. The idea is actually quite straightforward.